The highlights from Shippax 2026 - an update from the global Ferry Market

9. juni 2026

As part of the Norwegian Cruise & Ferry export initiative, we were present at the Shippax Ferry Conference 2026. This year's conference was held onboard the GNV Rhapsody during her voyage between Genoa and Sardinia, bringing together ferry operators, shipowners, shipyards, designers, equipment suppliers, and industry analysts from across Europe.

A total of 24 different Norwegian companies attended the conference, representing a broad cross-section of the maritime value chain, reflecting Norway's position as a leading supplier of innovative maritime solutions.

The Shippax conference has grown to be one of the most important meeting places for the international ferry community, bringing together operators, shipowners, shipyards, designers and equipment suppliers from across the world.

A key take away was that the European RoPax market is shifting. Not in one single direction, but with increasingly clear differences between regions, operators, and underlying market dynamics. We’ll explain some of the hightlights in this article.

The Mediterranean takes the lead while Northern Europe is flattening out

Mediterranean operators are strengthening their position. Companies such as Grimaldi Group, GNV, Attica Group and Baleària, Corsica Linea are picking up momentum, and also Scandinavian ship owner’s such as Stena Line and DFDS is increasingly focusing on the Medeteranian, where specially the traffic to North Africa is increasing. Grimaldi’s six vessel contract underlines this.

Within ro-ro and ro-pax, the shift is significant. The three largest European and Mediterranean short-sea ro-ro operators now control more than 30% of global ro-ro lane meter capacity. Growth is strongly linked to expanding connections between Europe and North Africa, with multiple new routes established in recent years.

In contrast, Northern Europe is showing signs of stagnation. Revenues for several ferry groups remained largely flat through 2025, and passenger numbers have not fully recovered to pre-pandemic levels.

Margins are also under pressure. Higher fuel costs, weaker demand and the effect of the war in Ukraine are squeezing profitability. EBIT margins appear to be flattening—or even thinning—for several operators.

Energy efficiency becomes the key battleground

What clearly cuts across regions is the increasing focus on energy efficiency. Fuel is no longer just a cost item, but becoming the core competitive parameter.

There are two parallel developments:

1. Operational optimisation

Operators are already achieving significant gains through smarter operations. P&O Ferries reported a 16% reduction in fuel consumption purely through behavioural and operational changes—better routing, speed optimisation, and data-driven decision-making.

This highlights a key shift where major efficiency gains can be unlocked without new vessels, simply by operating existing fleets more intelligently.

2. Newbuild efficiency

At the same time, new vessels are being designed with dramatically lower energy consumption in mind.

Corsica Linea has indicated that their planned new ferries could reduce fuel consumption by up to 30% compared to today’s vessels.

Another example of this focus we saw when visiting TT-Lines in Travemünde on the trade mission earlier this year, where focus on batteries and energy efficient solutions has become a key driver for their newbuilds in China.

Magne Ekerum, CDO Seat Innovation explains how Seat Innovation and Eknes now will join forces (Photo: Shippax)

Newbuildings: A Market Waiting for Renewal

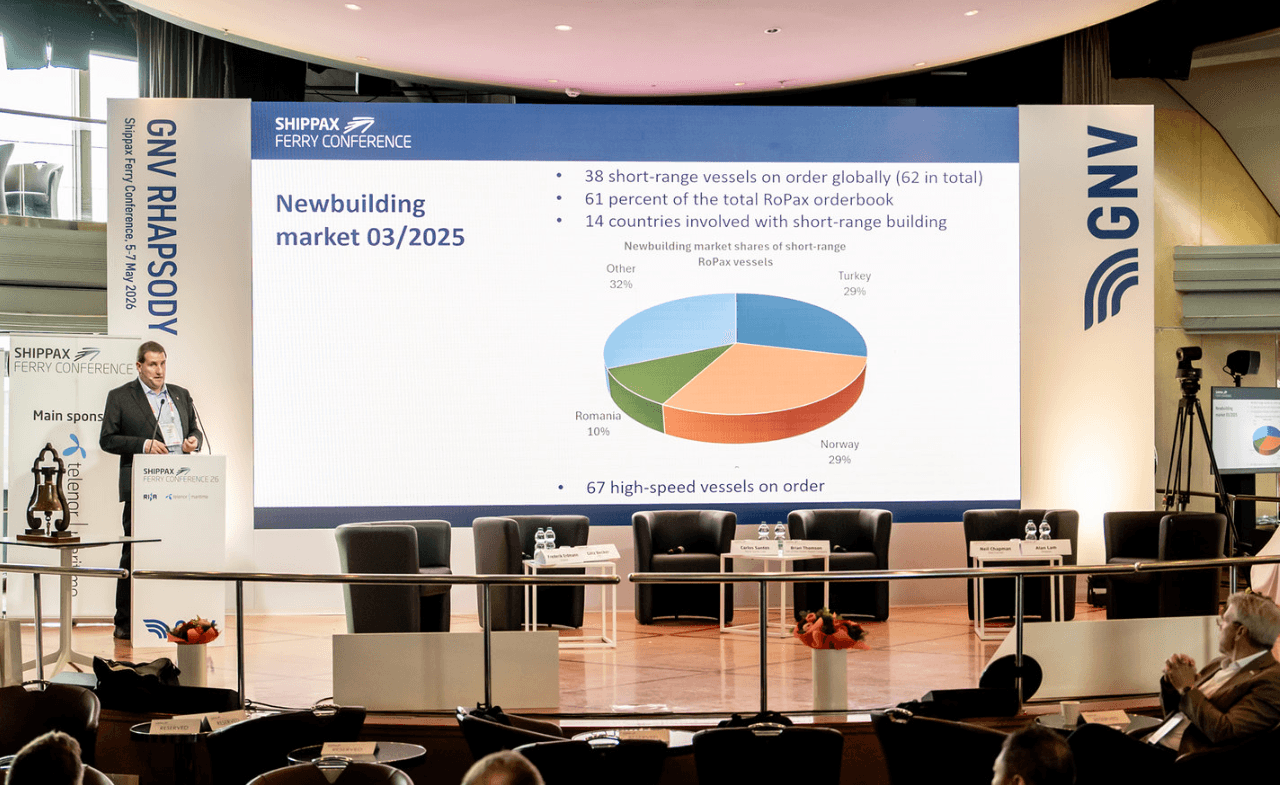

One of the more interesting observations from Shippax 2026 is the apparent contradiction between fleet age and newbuilding activity.

Globally, the ro-pax fleet consists of approximately 1,500 vessels with an average age of 25 years, while the shortsea ro-ro fleet averages 21 years. More notably, 351 ro-pax vessels and 148 ro-ro vessels currently in operation were built in 1990 or earlier. In most shipping segments, such fleet demographics would normally trigger a significant replacement cycle.Yet newbuilding activity remains subdued.

(Photo: Shippax)

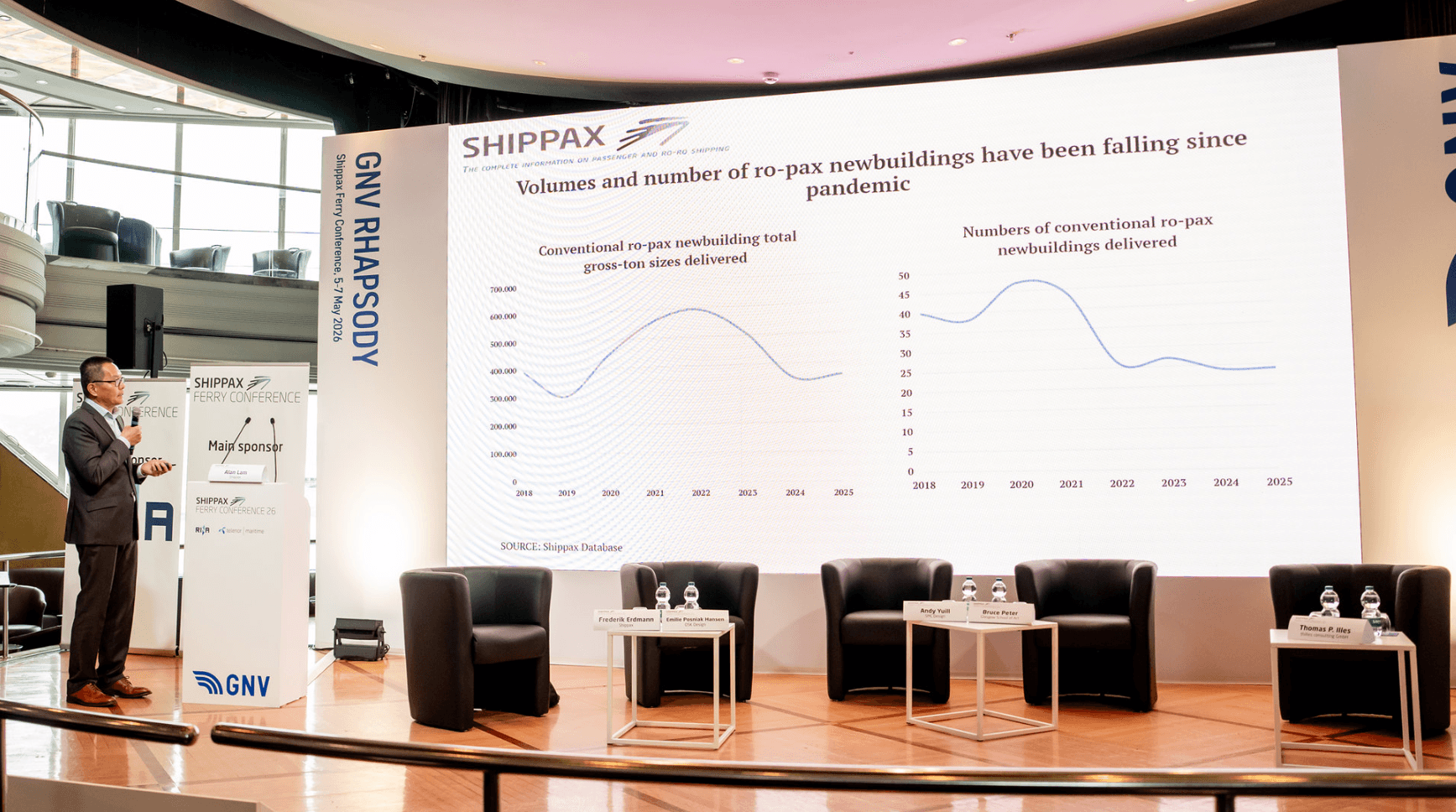

Since the pandemic, both the number of conventional ro-pax vessels delivered and the total gross tonnage entering the market have declined significantly. Deliveries peaked around 2020–2022 and have since fallen back to levels well below historical highs.

Several factors help explain this. High interest rates, uncertainty around future fuel choices, elevated shipbuilding prices, and geopolitical uncertainty have all contributed to delayed investment decisions. Many operators appear to be extending the life of existing vessels while waiting for greater clarity regarding technology pathways and regulatory developments.

China is dominating the RoPax Market

At the same time, the current orderbook reveals another striking trend: increasing concentration within shipbuilding. Two Chinese shipyards, CMI Jinling Weihai and GSI currently account for 76% of the ferry orderbook measured by gross tonnage. This underlines both the scale of Chinese shipbuilding competitiveness and the challenges faced by European yards in securing large ferry projects.

However, the underlying fundamentals suggest that fleet renewal cannot be postponed indefinitely. Ageing vessels, increasingly demanding environmental regulations, and rising operating costs will eventually force investment decisions. The question is therefore not whether renewal will happen, but when.

In the upcoming year, the rate of newbuilds in both the RoPax and RoRo market is believed to be quite stable.

(Photo: Shippax)

Still a market with a high growth potential for Norwegian suppliers

While the global ro-pax market is not traditionally where Norway holds its strongest position, it remains one of the most interesting growth opportunities for many Norwegian companies.

Norwegian companies are world-leading within electric ferries, energy systems, propulsion, automation, digital solutions, and operational optimisation. Many of the technologies developed for the Norwegian ferry market are now directly relevant to international operators facing increasing pressure to reduce emissions and operating costs.

For many years, discussions were dominated by CAPEX—new vessels, alternative fuels, and major investments. Increasingly, the conversation is moving towards OPEX.

EU ETS is starting to have a measurable impact on ferry operators in Europe and fuel costs remain a major concern. At the same time, operators are actively searching for ways to reduce consumption and improve efficiency The winners of the next decade may not necessarily be the operators with the newest ships or the largest fleets. They may be the operators that are best able to combine vessel design, digitalisation, operational excellence, and energy efficiency.

Due to the high amount of vessels being built in China, we do however believe the way to success for most Norwegian companies in the market is through the European Shipowner’s and designers.

As the industry shifts its focus from capacity growth to energy performance, many of the capabilities developed in Norway over the past decade become increasingly relevant to international ferry operators, both within newbuilds and retrofits.

For Norwegian suppliers this could mean more and good opportunities in a quite stable market!